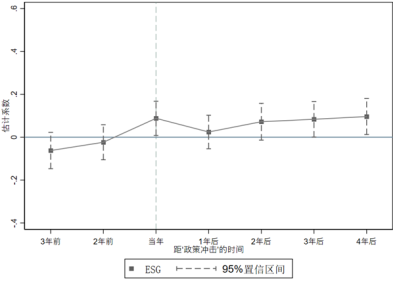

Against the backdrop of the gradual deepening of people’s democracy in the whole process, government information disclosure has become a key and fundamental institutional arrangement. It not only ensures citizens’ rights to know and participate, but also provides important support for the modernization of government governance. Government information disclosure can provide enterprises with authoritative, timely, and comparable public data, especially in areas such as environmental monitoring, social responsibility fulfillment, and corporate governance structure, significantly reducing the uncertainty of external information for enterprises. Such information helps firms identify their ESG shortcomings, optimize decision-making processes, and thus more effectively fulfill social responsibilities and improve overall ESG performance. Based on this, this paper selects panel data of A-share listed companies in Shanghai and Shenzhen from 2011 to 2021 as the research object, and employs a difference-in-differences model to systematically examine the causal effect of government information disclosure on corporate ESG performance. The findings indicate that government information disclosure has a significant positive impact on corporate ESG performance, with particularly prominent effects on environmental information disclosure and governance transparency. The government plays an indispensable role in promoting corporate ESG development and information disclosure, acting both as an information provider and a rule-maker. To further amplify the positive effects of government information disclosure, this paper proposes the following policy recommendations: first, establish and improve a policy framework and regulatory mechanism covering environmental, social, and governance dimensions, and strengthen the standardization and mandatory nature of information disclosure; second, fully utilize the internet and big data technologies to create a unified government information release platform, improving the accessibility and coverage of information; third, enhance public ESG awareness through public guidance and supervision, forcing enterprises to proactively improve their ESG performance. Ultimately, the goal is to build a healthy, transparent, and sustainable business environment, and to promote the implementation of people’s democracy in the whole process in the economic and social fields.

| Published in | Science Innovation (Volume 14, Issue 2) |

| DOI | 10.11648/j.si.20261402.11 |

| Page(s) | 15-24 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Government Information Disclosure, Corporate ESG, Corporate Life Cycle

变量 | 变量名称 | 个数 | 平均值 | 标准差 | 最小值 | 最大值 |

|---|---|---|---|---|---|---|

ESG | ESG | 29038 | 4.138 | 1.040 | 1 | 8 |

GT | 政府信息公开 | 29370 | 0.087 | 0.281 | 0 | 1 |

Roa | 总资产净利润率 | 29370 | 0.039 | 0.063 | -0.432 | 0.214 |

Tang | 资产结构 | 29169 | 0.355 | 0.174 | 0.014 | 0.829 |

Tl | 总负债率 | 29370 | 0.419 | 0.206 | 0.032 | 1.100 |

Cflow | 现金流量 | 29369 | 0.048 | 0.067 | -0.206 | 0.252 |

Size | 企业规模 | 29370 | 22.190 | 1.302 | 19.29 | 26.520 |

Lnage | 企业年龄 | 29354 | 2.054 | 0.907 | 0 | 3.367 |

(1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

ESG | ESG | ESG | ESG | ESG | ESG | ESG | |

GT | 0.0766*** | 0.0873*** | 0.0904*** | 0.0938*** | 0.0936*** | 0.0853*** | 0.0766*** |

(0.0238) | (0.0238) | (0.0240) | (0.0238) | (0.0238) | (0.0237) | (0.0235) | |

Roa | 0.9746*** | 0.8778*** | 0.5651*** | 0.6645*** | 0.4236*** | 0.3247*** | |

(0.1007) | (0.1032) | (0.1063) | (0.1090) | (0.1064) | (0.1059) | ||

Tang | -0.3772*** | -0.2525*** | -0.2539*** | -0.1192** | 0.0109 | ||

(0.0530) | (0.0538) | (0.0538) | (0.0531) | (0.0533) | |||

Tl | -0.5915*** | -0.5896*** | -0.9274*** | -0.7449*** | |||

(0.0499) | (0.0499) | (0.0522) | (0.0528) | ||||

cflow | -0.4350*** | -0.3942*** | -0.3153*** | ||||

(0.0853) | (0.0841) | (0.0832) | |||||

Size | 0.2531*** | 0.2854*** | |||||

(0.0134) | (0.0135) | ||||||

Lnage | -0.3039*** | ||||||

(0.0169) | |||||||

_cons | 4.1314*** | 4.0928*** | 4.2333*** | 4.4499*** | 4.4665*** | -1.0514*** | -1.2569*** |

(0.0045) | (0.0059) | (0.0203) | (0.0278) | (0.0279) | (0.2925) | (0.2919) | |

时间 | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

年份 | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

行业 | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

县级 | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

N | 28565 | 28565 | 28377 | 28377 | 28376 | 28376 | 28375 |

R2 | 0.644 | 0.646 | 0.647 | 0.649 | 0.650 | 0.657 | 0.661 |

(1) | (2) | (3) | |

|---|---|---|---|

替换被解释变量 | 工具变量法 | ||

ESG2 | 第一阶段 | 第二阶段 | |

GT | 0.0698*** | 38.5501*** | |

(0.0254) | (10.3883) | ||

IV | 0.0110*** | ||

(0.0030) | |||

Kleibergen-Paap rk LM statistic | 16.117*** | ||

Hansen J statistic | 0.000 | ||

控制变量 | Yes | Yes | Yes |

时间 | Yes | Yes | Yes |

年份 | Yes | Yes | Yes |

行业 | Yes | Yes | Yes |

县级 | Yes | Yes | Yes |

N | 28375 | 25087 | |

R2 | 0.628 | ||

(1) | (2) | |

|---|---|---|

国有企业 | 非国有企业 | |

ESG | ESG | |

GT | 0.1041*** | -0.0175 |

(0.0324) | (0.0343) | |

控制变量 | Yes | Yes |

时间 | Yes | Yes |

年份 | Yes | Yes |

行业 | Yes | Yes |

县级 | Yes | Yes |

N | 10396 | 17710 |

R2 | 0.711 | 0.655 |

(1) | (2) | (3) | |

|---|---|---|---|

成长期 | 成熟期 | 衰退期 | |

ESG | ESG | ESG | |

GT | 0.1552*** | 0.0731 | 0.0354 |

(0.0571) | (0.0574) | (0.0396) | |

控制变量 | Yes | Yes | Yes |

时间 | Yes | Yes | Yes |

年份 | Yes | Yes | Yes |

行业 | Yes | Yes | Yes |

县级 | Yes | Yes | Yes |

N | 8155 | 7295 | 10482 |

R2 | 0.709 | 0.736 | 0.719 |

| [1] | 于文超, 梁平汉. 不确定性、营商环境与民营企业经营活力 [J]. 中国工业经济, 2019, (11): 136-154. |

| [2] | 于文超, 梁平汉, 高楠. 公开能带来效率吗?——政府信息公开影响企业投资效率的经验研究 [J]. 经济学(季刊), 2020, 19(03): 1041-1058. |

| [3] | 于文超, 王丹. 政府信息公开、政策不确定性与企业盈余管理 [J]. 产业经济研究, 2022, (03): 100-112+142. |

| [4] | 郑思尧, 孟天广. 公共危机治理中的政府信息公开与治理效度——基于一项调查实验 [J]. 公共管理与政策评论, 2022, 11(01):88-103. |

| [5] | 姜艳. 公众使用社交媒体、政府透明度与政府信任——基于网民社会意识调查的实证研究 [J]. 社会科学家, 2023(07): 127-133. |

| [6] | Cheng B, Ioannou I, Serafeim G, Corporate Social Responsibility and Access to Finance [J]. Strategic Management Journal, 2014, 35(1): 1-23. |

| [7] | Ashwin Kumar N C, Smith C, Badis L, et al. ESG Factors and Risk-adjusted Performance: A New Quantitative Model [J]. Journal of Sustainable Finance & Investment, 2016, 6(4): 292-300. |

| [8] | 邱牧远, 殷红. 生态文明建设背景下企业ESG表现与融资成本 [J]. 数量经济技术经济研究, 2019, 36(03): 108-123. |

| [9] | 李井林, 阳镇, 陈劲, 等. ESG促进企业绩效的机制研究——基于企业创新的视角 [J]. 科学学与科学技术管理, 2021, 42(09): 71-89. |

| [10] | 陈洪涛, 何任翔, 高小然等. 券商公众号报道对企业ESG表现的影响研究 [J/OL]. 管理学报, 2023, 20(11): 1-9. |

| [11] | 唐莹, 肖洋. ESG表现对企业风险的影响效应研究 [J]. 山东工商学院学报, 2023, 37(05): 67-77. |

| [12] | 宋佳, 张金昌, 潘艺. ESG发展对企业新质生产力影响的研究——来自中国A股上市企业的经验证据 [J]. 当代经济管理, 2024, 46(06): 1-11. |

| [13] | 李逸飞. 增值税留抵退税与企业人力资本升级 [J]. 世界经济, 2023, 46(12): 115-140. |

| [14] | 谢红军, 吕雪. 负责任的国际投资: ESG与中国OFDI [J]. 经济研究, 2022, 57(03): 83-99. |

| [15] | 毛其淋, 王玥清. ESG的就业效应研究: 来自中国上市公司的证据 [J]. 经济研究, 2023, 58(07): 86-103. |

| [16] | Lin Y, Fu X, Fu X. Varieties in state capitalism and corporate innovation: Evidence from an emerging economy [J]. Journal of Corporate Finance, 2021, 67: 101919. |

| [17] | Song Y, Wu H, Ma Y. Does ESG performance affect audit pricing? Evidence from China [J]. International Review of Financial Analysis, 2023, 90: 102890. |

| [18] | Ye X, Hou R, Wang S, et al. Social Media, Relationship Marketing and Corporate ESG Performance [J]. Finance Research Letters, 2024: 105288. |

| [19] | Shin J, Moon J J, Kang J. Where does ESG pay? The role of national culture in moderating the relationship between ESG performance and financial performance [J]. International Business Review, 2023, 32(3): 102071. |

| [20] | 方先明, 胡丁. 企业ESG表现与创新——来自A股上市公司的证据 [J]. 经济研究, 2023, 58(02): 91-106. |

| [21] | 蔡贵龙, 张亚楠. 基金ESG投资承诺效应——来自公募基金签署PRI的准自然实验 [J]. 经济研究, 2023, 58(12): 22-40. |

APA Style

Peng, Q. (2026). Analysis of Impact of Government Information Disclosure on Corporate ESG Performance —— Taking A-Share Listed Companies in Shanghai and Shenzhen as an Example. Science Innovation, 14(2), 15-24. https://doi.org/10.11648/j.si.20261402.11

ACS Style

Peng, Q. Analysis of Impact of Government Information Disclosure on Corporate ESG Performance —— Taking A-Share Listed Companies in Shanghai and Shenzhen as an Example. Sci. Innov. 2026, 14(2), 15-24. doi: 10.11648/j.si.20261402.11

@article{10.11648/j.si.20261402.11,

author = {Qifei Peng},

title = {Analysis of Impact of Government Information Disclosure on Corporate ESG Performance —— Taking A-Share Listed Companies in Shanghai and Shenzhen as an Example},

journal = {Science Innovation},

volume = {14},

number = {2},

pages = {15-24},

doi = {10.11648/j.si.20261402.11},

url = {https://doi.org/10.11648/j.si.20261402.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.si.20261402.11},

abstract = {Against the backdrop of the gradual deepening of people’s democracy in the whole process, government information disclosure has become a key and fundamental institutional arrangement. It not only ensures citizens’ rights to know and participate, but also provides important support for the modernization of government governance. Government information disclosure can provide enterprises with authoritative, timely, and comparable public data, especially in areas such as environmental monitoring, social responsibility fulfillment, and corporate governance structure, significantly reducing the uncertainty of external information for enterprises. Such information helps firms identify their ESG shortcomings, optimize decision-making processes, and thus more effectively fulfill social responsibilities and improve overall ESG performance. Based on this, this paper selects panel data of A-share listed companies in Shanghai and Shenzhen from 2011 to 2021 as the research object, and employs a difference-in-differences model to systematically examine the causal effect of government information disclosure on corporate ESG performance. The findings indicate that government information disclosure has a significant positive impact on corporate ESG performance, with particularly prominent effects on environmental information disclosure and governance transparency. The government plays an indispensable role in promoting corporate ESG development and information disclosure, acting both as an information provider and a rule-maker. To further amplify the positive effects of government information disclosure, this paper proposes the following policy recommendations: first, establish and improve a policy framework and regulatory mechanism covering environmental, social, and governance dimensions, and strengthen the standardization and mandatory nature of information disclosure; second, fully utilize the internet and big data technologies to create a unified government information release platform, improving the accessibility and coverage of information; third, enhance public ESG awareness through public guidance and supervision, forcing enterprises to proactively improve their ESG performance. Ultimately, the goal is to build a healthy, transparent, and sustainable business environment, and to promote the implementation of people’s democracy in the whole process in the economic and social fields.},

year = {2026}

}

TY - JOUR T1 - Analysis of Impact of Government Information Disclosure on Corporate ESG Performance —— Taking A-Share Listed Companies in Shanghai and Shenzhen as an Example AU - Qifei Peng Y1 - 2026/04/21 PY - 2026 N1 - https://doi.org/10.11648/j.si.20261402.11 DO - 10.11648/j.si.20261402.11 T2 - Science Innovation JF - Science Innovation JO - Science Innovation SP - 15 EP - 24 PB - Science Publishing Group SN - 2328-787X UR - https://doi.org/10.11648/j.si.20261402.11 AB - Against the backdrop of the gradual deepening of people’s democracy in the whole process, government information disclosure has become a key and fundamental institutional arrangement. It not only ensures citizens’ rights to know and participate, but also provides important support for the modernization of government governance. Government information disclosure can provide enterprises with authoritative, timely, and comparable public data, especially in areas such as environmental monitoring, social responsibility fulfillment, and corporate governance structure, significantly reducing the uncertainty of external information for enterprises. Such information helps firms identify their ESG shortcomings, optimize decision-making processes, and thus more effectively fulfill social responsibilities and improve overall ESG performance. Based on this, this paper selects panel data of A-share listed companies in Shanghai and Shenzhen from 2011 to 2021 as the research object, and employs a difference-in-differences model to systematically examine the causal effect of government information disclosure on corporate ESG performance. The findings indicate that government information disclosure has a significant positive impact on corporate ESG performance, with particularly prominent effects on environmental information disclosure and governance transparency. The government plays an indispensable role in promoting corporate ESG development and information disclosure, acting both as an information provider and a rule-maker. To further amplify the positive effects of government information disclosure, this paper proposes the following policy recommendations: first, establish and improve a policy framework and regulatory mechanism covering environmental, social, and governance dimensions, and strengthen the standardization and mandatory nature of information disclosure; second, fully utilize the internet and big data technologies to create a unified government information release platform, improving the accessibility and coverage of information; third, enhance public ESG awareness through public guidance and supervision, forcing enterprises to proactively improve their ESG performance. Ultimately, the goal is to build a healthy, transparent, and sustainable business environment, and to promote the implementation of people’s democracy in the whole process in the economic and social fields. VL - 14 IS - 2 ER -

School of Business, East China University of Political Science and Law, Shanghai, China